It is not uncommon for corporations to own stock in other corporations. The ownership could be either through an acquisition or the creation of a new corporation by the parent company. Sometimes, for various reasons, the parent company wants to separate their ownership in the subsidiary corporation, most of the time it’s because the subsidiary is in an unrelated business from the parent or the subsidiary has more growth prospects as a separate company from the parent. That separation from the parent corporation can be either through a spin-off, split-off, split-up, carve-out, or simply a sale of the subsidiary. This article will focus on the first three and briefly discuss a carve-out; a sale of a corporation is straightforward and will not be covered.

What is a corporate Spin-Off?

First let’s define what is a corporate spin-off; a corporate spin-off is when a new company is created from the subsidiary or division of an existing (parent) company. The parent company creates a completely separate entity and issues new shares of the new entity to its existing shareholders. A spin-off is also known as a divestiture. One of the most prominent examples was the spin-off of PayPal (PYPL) from its former parent EBay (EBAY) on July 17, 2015. In that case, EBay shareholders received one share of PayPal for each share of EBay they owned. EBay recognized the growth potential of PayPal as an independent company and made the following announcement “each [company will] have a sharper focus and greater flexibility to pursue future success in their respective global commerce and payments markets.” In a spin-off, existing shareholders do not give up or exchange any of their existing shares in the parent company. They essentially receive shares of the new company on a pro-rata basis; this pro-rata allocation also allows for a non-taxable event (see below for tax implications).

What is a corporate Split-Off?

What is a corporate split-off and what is the difference between a spin-off and split-off? A corporate split-off is when a new entity is created from the parent company and shareholders of the parent company exchange their shares for the newly created entity. One notable example is the split-off of Synchrony Financial (SYF) from its parent General Electric (GE) on November 17, 2015. Synchrony Financial was a wholly owned subsidiary of General Electric, but then CEO Jeffrey Immelt decided to separate its financial business from its core industrial business. In that announcement, GE offered its existing shareholders the opportunity to exchange each share of GE stock for 1.0505 shares of newly formed Synchrony stock. The key words here are opportunity and exchange; as you can see, the main difference between a spin-off and a split-off is that in a split-off, shareholders must exchange their existing shares for the new company whereas in a spin-off, the existing shareholders are given shares in the new company. Also, shareholders of the parent company are not required to exchange their shares; they have the opportunity to do so and can choose to keep their existing shares of the parent company. Lastly, don’t assume the spin-off is better because the shareholder is given shares versus having to exchange their existing shares; in a spin-off, the market value of the parent corporation declines by the market value of the spun off corporation.

What is a corporate Split-Up?

In the previous two examples, the parent company either gives shares of a new company to existing shareholders or allows existing shareholders to exchange their shares for the new company. In both instances, the parent company survives as a standalone company. In a split-up, the parent company is split into two or more entities, but the parent company is liquidated and does not survive. The largest most recent example is the announcement by United Technologies on November 26, 2018 to split-up into three separate companies: United Technologies, Otis Elevator Company, and Carrier. While the United Technologies name will remain the same for one of the three companies, the new company (UTC) will be an entirely new entity from its original parent (UTX).

Sometimes the government intervenes and forces a company to split-up. This actually happened in 1984 when the US Justice Department deemed AT&T a monopoly and forced it to break-up into 8 different smaller companies. In current news, there is growing public consensus that some technology companies have grown too big and wield too much control over our day to day lives. As a result, there is public pressure to classify Amazon, Google, and Apple as monopolies and for the government to step-in to break them up. We shall see how that story unfolds.

What is a Carve-Out?

Another corporate action is a carve-out which is essentially when a parent company creates a new corporation and sells shares of that new corporation through an IPO (Initial Public Offering). No shares are given to or exchanged with existing shareholders. The newly issued shares from the IPO are essentially available for anyone to purchase, including existing shareholders of the parent company. In 2009, Las Vegas Sands did a carve-out of its Sands China subsidiary into a new entity to raise over $3 billion in cash. According to Deloitte Corporate Finance, 64 percent of companies engage in carve outs because they need cash or capital. The number one reason is because the entity is “not considered core to the [parent] company’s business strategy.”

What is the cost basis after a corporate Spin-Off or Split-Off?

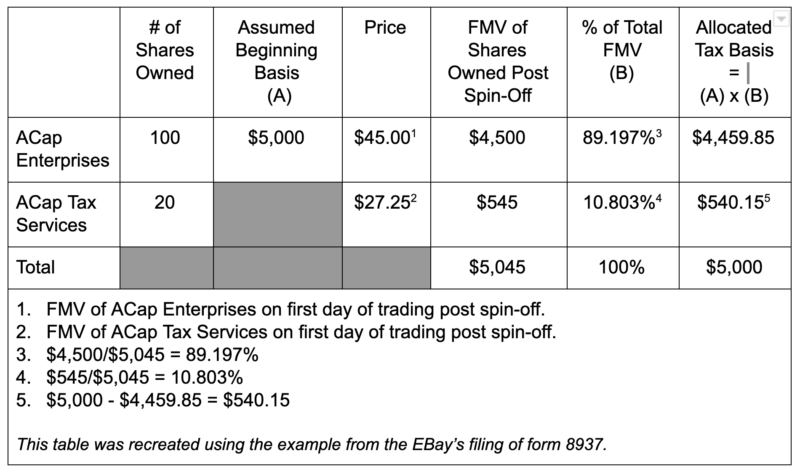

As with any corporate action, it is important to understand the tax implications, especially cost-basis which is the key variable when calculating capital gains taxes. The taxation of spin-offs, split-offs, and split-ups is governed by Internal Revenue Code 355 (IRC 355). Generally speaking, such events are not taxable when they occur if the company follows certain rules, which are beyond the scope of this article. The most important question to ask is what is my cost basis after a spin-off, split-off, or split-up? Below is a simple fictitious example to help understand how to calculate the cost basis after a corporate reorganization assuming a one-time purchase of 100 shares in ACap Enterprises (AE) for $5,000 and the subsequent spin-off of ACap Tax Services (ATS) where AE shareholders are given 1 share of ATS for each share of AE they own.

The examples above assume simple reorganizations with whole shares, but is not always the case. There are many other situations that may arise; for example, there could be fractional shares issued, cash in lieu of fractional shares, reinvested dividends, stock splits, and shares purchased over a period of time all result in differing cost basis. As a result, cost basis and capital gain taxes become very complicated. If you own stock in any company, you will at some point experience a corporate reorganization. While you may ignore the proxy materials mailed to you to vote on the matter, the end result will still affect how much you pay in taxes so it is imperative to keep meticulous records.

Looking for an independent fiduciary financial advisor who can advise you on investments, retirement, real estate, alternative assets, and taxes? Contact ACap Advisors & Accountants to schedule a free initial consultation. Our clients include individuals, small businesses, entrepreneurs, and anyone serious about saving and investing for their future.

Ara Oghoorian, CFA, CFP, CPA is the founder and president of ACap Advisors & Accountants in Los Angeles, CA.